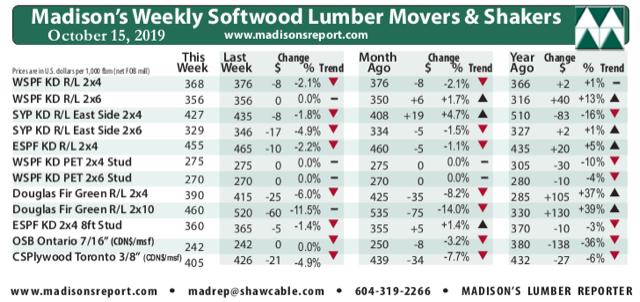

Last week Western Spruce-Pine-Fir KD 2x4 #2&Btr lost -$8, or -2%, to close at US$368 mfbm. Last week's price is also -$8 less than it was one month ago. Compared to one year ago, this price is up +$2. Demand and prices were generally flat to down, in both lumber and panels.

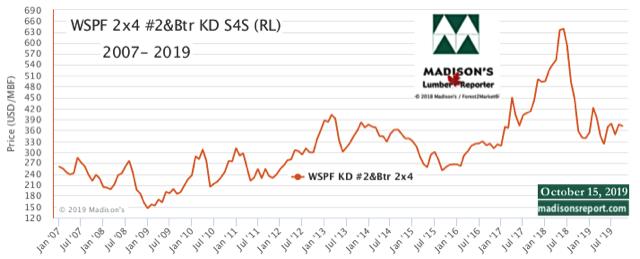

Compared to historical trend, last week's WSPF 2x4 #2&Btr price is up +$6, or almost +2%, relative to the 1-year rolling average price of US$362 mfbm, and is down -$77, or -17%, relative to the 2-year rolling average price of US$445 mfbm. Traders of WSPF lumber in the US had hoped demand would pick up some steam after a lackluster kickoff to October, but lumber purveyors found every transaction was a bit of a fight.

Buyers of WSPF lumber in the US remained reticent and cautious even as their already-low inventories ran down further. Two-week order files were common for sawmills. Transportation was relatively smooth in the Western United States and secondary suppliers often had decent tallies available for quick shipment. Customers didn’t feel any pressure to act quickly or secure large volumes. Meanwhile in Canada, producers of WSPF commodities sold a bit each day but demand overall left much to be desired considering the time of year. Despite solid construction activity persisting in many regions of both the US and Canada, buyers were slow to make deals and continued to purchase scant volumes. Low transit volumes made shipments more timely and helped customers hold off buying when they wanted to. Currently customers are confident that when downstream orders materialize they will be able to get what they need from either sawmills or wholesalers in a timely fashion.

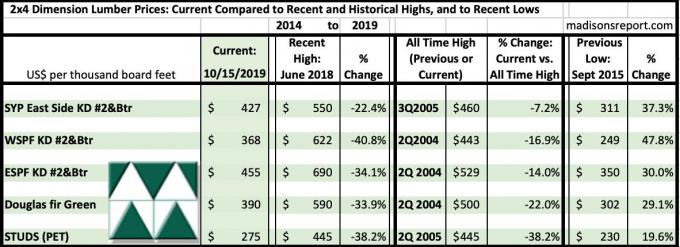

The below table is a comparison of recent highs, in June 2018, and current October 2019 benchmark dimension softwood lumber 2x4 prices compared to historical highs of 2004/05 and compared to recent lows of Sept 2015: