In 2023, North America's net sawmill capacity decreased by 2%, triggered by diminishing lumber demand and past overproduction issues, according to a report by Russ Taylor Global. This trend has led to the permanent closure of nine sawmills and reductions in shifts, particularly in British Columbia (BC) and the US South, where economic pressures have also forced mills to shut down to balance timber supplies.

Throughout the last six to seven years, substantial expansions and the establishment of new mills, primarily in the US South, added significant capacity. These were partly offset by closures mainly in BC and the US West. However, recent closures, including unexpected ones in the US South, have intensified as lumber prices fell below break-even points in several areas during 2023. Moving into 2024, the sector saw three new mills starting operations in the US South, while nine additional sawmills across North America announced closures.

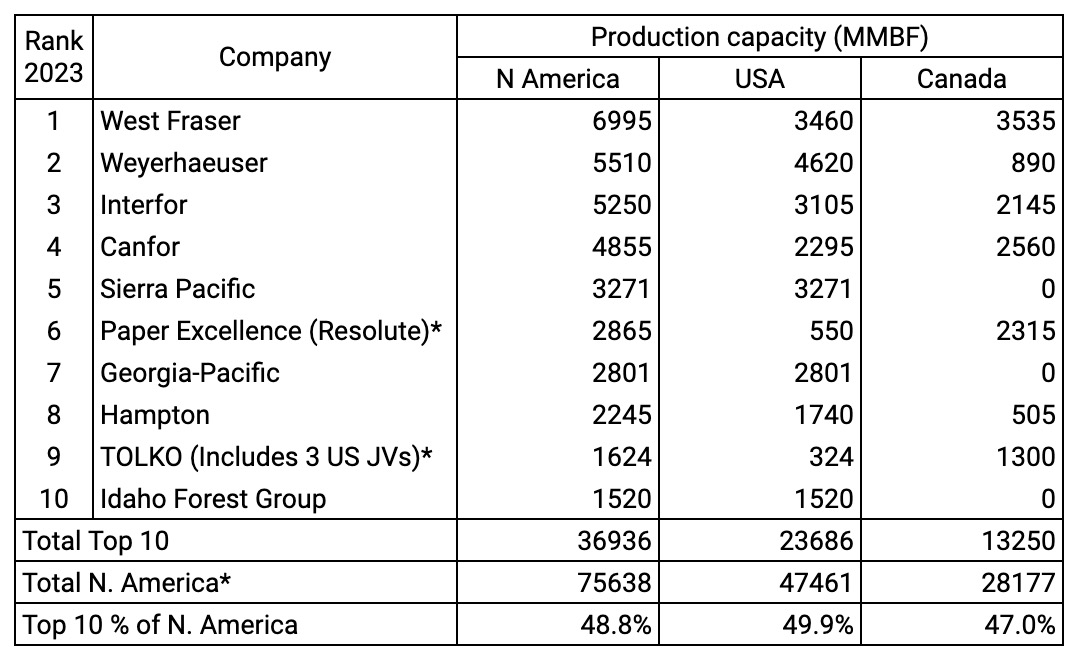

Forisk's analysis highlighted that the top ten softwood lumber producers in North America held about 49% of the total capacity, amounting to 36.9 billion board feet in 2023. West Fraser topped this list with a capacity of 7 billion board feet. In the US, Weyerhaeuser led with 4.6 billion board feet, representing around 50% of the US total alongside other major producers.

The lumber market experiences its seasonal peak around April, yet this pattern shifted drastically in the past two years. In 2024, Western Spruce-Pine-Fir (W-SPF) lumber prices have shown improvement, slightly surpassing their 2023 high in March. However, Southern Yellow Pine (SYP) has been trading at significant discounts, unusual in historical comparisons, stressing the financial viability of mills in the US South.

In terms of pricing, Western Spruce-Pine-Fir (W-SPF) saw prices starting at US$400s in early 2024, peaking at US$460 per thousand board feet (MBF) in March, a slight increase from 2023. Conversely, Southern Yellow Pine (SYP) prices dramatically dropped, trading at a US$120 per MBF discount to W-SPF in mid-April 2024 — a stark contrast to its usual premium. This significant price disparity has led to financial strains on SYP mills, prompting temporary and permanent closures in the US South.

The disparities extend to other softwood varieties. In mid-April, Fir-Larch and Hemlock-Fir in the US Inland region recorded prices around US$525 and US$520 per MBF respectively, maintaining substantial premiums over both W-SPF and SYP.

Market adjustments have been stark in BC, where high costs and limited log availability have pushed prices below sustainable levels, prompting further mill curtailments. Bild: Top N. America Softwood Lumber Producers / Forisk NA Forest Industry Capacity Database / Russ Taylor Global

* US & Canada volumes - Estimated

In the United States, the lumber market is expected to remain relatively stable compared to other global markets in 2024. High mortgage rates and a limited inventory of existing homes are benefiting new residential construction, which is a crucial demand driver for lumber. Predictions suggest that the number of new single-family homes, which use significantly more lumber than multi-family units, will increase in 2024.

Conversely, in Europe, China, and Japan, lumber demand has weakened due to oversupply, high interest rates, and low consumer confidence. The global lumber market is struggling with too much supply and insufficient demand, leading to flat or declining prices. However, there is a hopeful outlook for improvement in the second half of 2024, with some regions possibly seeing a slight uptick in demand if supply issues are addressed effectively.