The first full back-to-work / school week for September 2019 did not bode well for North American construction framing softwood lumber prices, said Madison’s Lumber Reporter. While wholesaler prices of many wood home building materials stayed flat, and there were two panel mill and one sawmill curtailment announcement, overall demand was not encouraging for an improving market before winter sets in.

Due to production cuts, many operators — at sawmills and plywood and OSB producers as well — were able to get their order files to longer than one week.

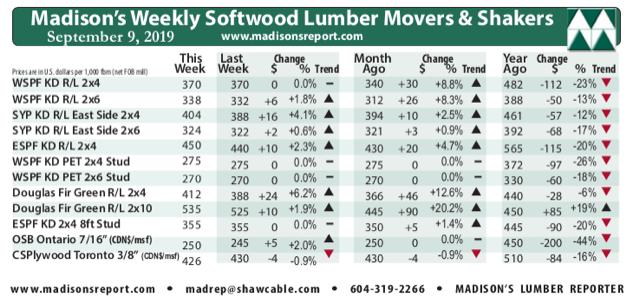

This week benchmark lumber commodity Western Spruce-Pine-Fir KD 2×4 #2&Btr price remained unchanged from the previous week, to close again at US$370 mfbm. One month ago this price was falling, hard. That may have stopped as, by comparison, this week’s price is up +$30, or +9%, from one month ago. Compared to one year ago, this price is down -$112, or -23%.

Compared to historical trend, this week’s Western SPF KD 2×4 #2&Btr prices are up +$3 relative to the 1-year rolling average price of US$367 mfbm. This price is down -$77, or -17%, relative to the 2-year rolling average price of $447.

Eastern stocking wholesalers, working mostly out of New Jersey, noted that sales were better this week, and while prices still weren’t optimal they at least appeared to be on an upward trajectory. Oriented Strand Board and plywood prices were up along the Eastern Seaboard due to apprehensions about Hurricane Dorian. Meanwhile, vendors in the US Northeast benefitted from producers’ current low supply levels, selling old, weathered lumber to desperate customers.

Still in panels, secondary suppliers of Eastern Spruce-Pine-Fir plywood in Canada reported good business out of their yards as buyers got back to the table on Tuesday. Plywood mill order files in the East ranged from September 16th to the 23rd. Sales of Oriented Strand Board finally showed some life thanks to reduced volumes coming in from the US Northeast and North Central regions. Low inventories ensured frequent participation from customers, and OSB mill order files were between September 16th and early October.

Western Spruce-Pine-Fir panel vendors again navigated a “frustrating market” this week. Selling OSB in the west was brutal, and secondary suppliers were tempted to just let their inventories run down to the pavement rather than continue taking precipitous losses. Plywood sales were weak as well; and despite whittling down order files to next week, plywood producers in the west refused to budge on pricing.

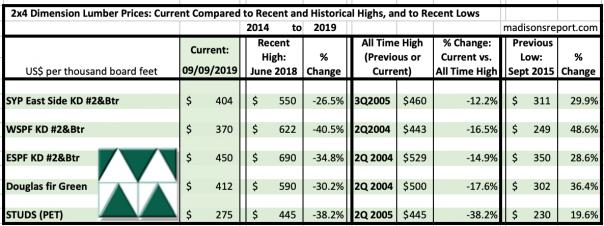

The below table is a comparison of recent highs, in June 2018, and current September 2019 benchmark dimension softwood lumber 2×4 prices compared to historical highs of 2004/05 and compared to recent lows of Sept 2015.