The historic climb for U.S. lumber prices, combined with delays and higher costs for other building materials, is a significant limiting factor for home building in 2021. Despite a historically diminished level of overall housing inventory and solid demand due to low mortgage interest rates and demographics, new construction has been limited in its ability to add needed supply to the market, resulting in unsustainable gains for home prices. Fortunately, real-time data indicate that lumber prices are now falling with an expectation that prices will decline below $1000 per thousand board feet in the coming weeks, as the National Association of Home Builders (NAHB) reported.

The following data track estimates concerning the sawmill industry (NAICS 3211). The data indicate that domestic production did not keep pace with the gains for home construction during an extraordinary 2020.

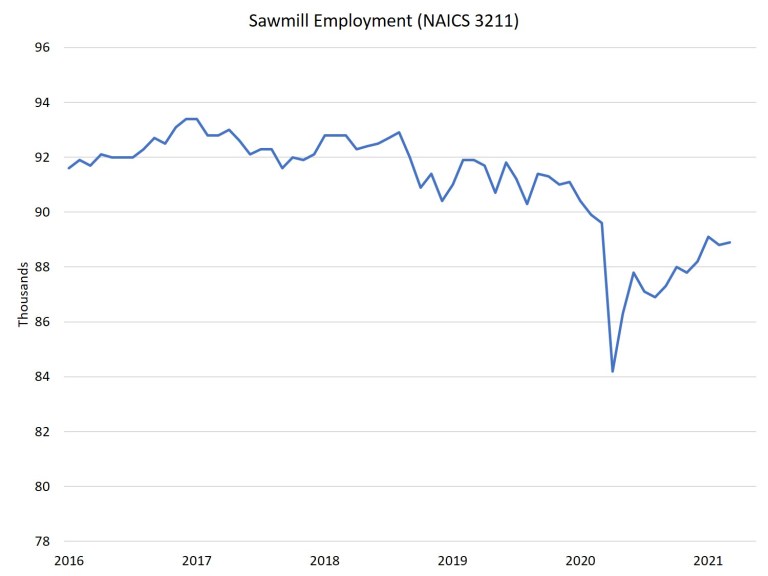

A cited reason for the lack of lumber production in the U.S. has been challenges with labor, a limiting factor for the overall economy in both the manufacturing and construction sectors. Bureau of Labor Statistics data indicate that, indeed, sawmill industry employment is lower than a year ago. As of March 2021, the most recent data available, sawmill employment was 88,900. This is a 0.8% decline from March 2020, or a net loss of 700 jobs. In contrast, residential construction employment was up 2.8%, or 82,000 net jobs over the same period.

Despite the decline in workers, sawmill output was flat over the course of 2020, albeit along a choppy trend. Revised data from the Federal Reserve demonstrate that the seasonally adjusted rate of sawmill output in March 2021 (the most recent available) was 4% higher than that recorded in March 2020, when the spring decline for production began last year. March 2021 saw a 4.4% gain over February 2021, due in part to a post-Winter Storm Uri rebound.

Looking back, total 2020 sawmill output was up just 0.1% higher compared to 2019. This was due to an upswing in production in November and December, which followed a decline in the 3Q.

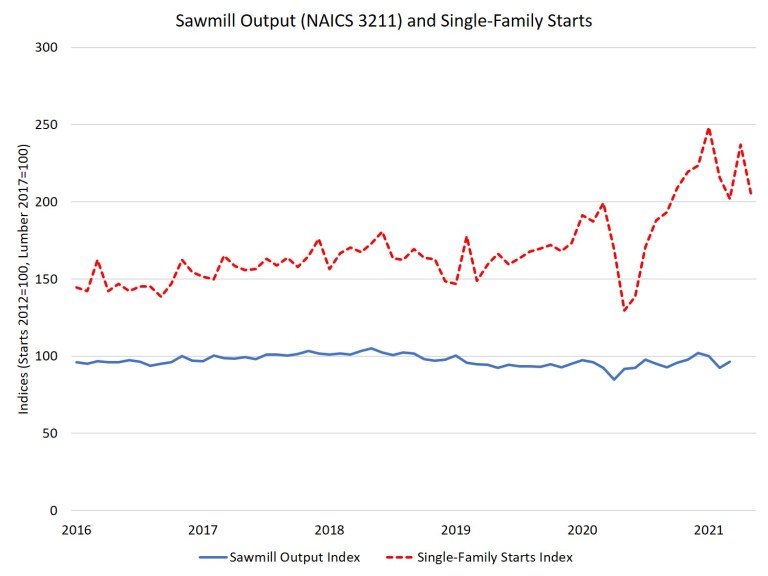

It worth noting that on a seasonally adjusted basis, the high point for U.S. sawmill output was May 2018. Output is down 8% since that time despite substantial price gains.

The 2020 output levels were insufficient to keep up with the demand from residential construction. The preceding graph presents single-family starts and sawmill output indexed so that 2012 housing starts / 2017 sawmill output levels equal 100. The growing gap between the two measures, particularly in 2020 when single-family starts expanded by 12%, is a reason for the dramatic increase in lumber prices.

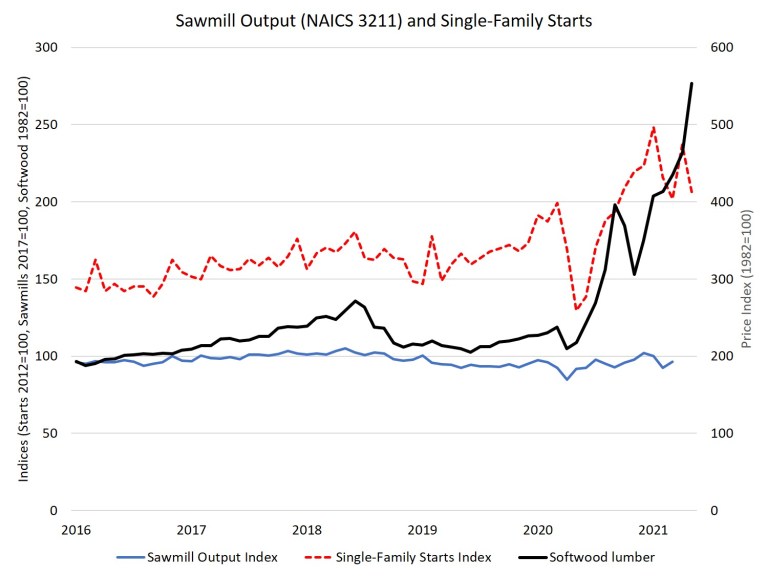

This impact on price can be seen above by adding an indexed measure of the BLS Producer Price Index for softwood lumber. These data indicate that the rise in price was due, in part, to the inability of lumber production to keep pace with residential construction expansion. This gap, and the material cost impact, can only be closed via a significant increase in domestic production, more U.S. imports of lumber, or a significant substitution to other building materials. Fortunately, lumber prices are now expected to decline in the weeks ahead, as indicated by recent activity in future markets.